Why AI Implementation Fails in a Mortgage Brokerage (And What to Do Instead)

Most mortgage brokerages that have tried AI will tell you the same thing: they set up ChatGPT, used it for a week, and it didn't change much. Some moved on. Others concluded AI wasn't ready for their kind of business.

They're not wrong that something failed. They're wrong about why.

The problem isn't the technology. The problem is that dropping a general-purpose AI tool into a brokerage and hoping it saves time is like handing someone a power drill and hoping they build a house. The tool is capable. The approach isn't.

Here's what actually goes wrong, and what firms that get real results from AI for mortgage brokers do differently.

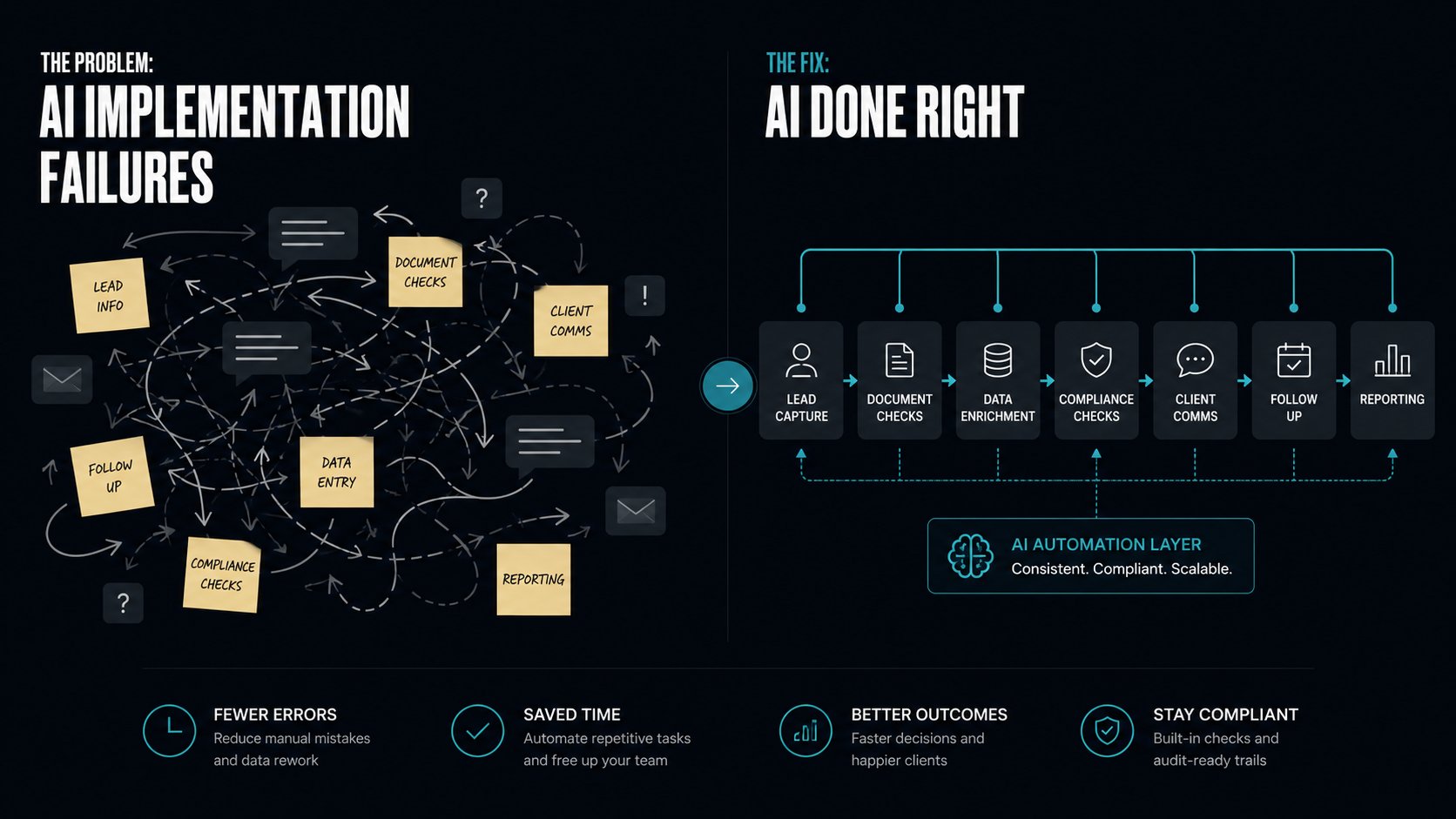

The ChatGPT Trap

The most common starting point for AI in a mortgage brokerage is a free ChatGPT account and good intentions.

Someone on the team uses it to draft a client email. It works reasonably well. A few others try it for research or to summarise a document. Useful enough. Then it sits mostly unused because nobody is quite sure how to work it into the daily flow, and the business carries on as before.

This isn't laziness or lack of imagination. It's a structural problem. ChatGPT is a general-purpose tool with no knowledge of your CRM, your case pipeline, your lender criteria, or your compliance obligations. It doesn't know what happened in your business yesterday and it has no way of knowing what needs to happen tomorrow. Asking it to improve a mortgage brokerage's operations without connecting it to the brokerage's actual data is like asking a consultant to improve your processes without letting them look at them.

The firms that get meaningful results from AI don't start with a tool. They start with a problem.

The Mistake of Starting With the Tool

When a brokerage decides to "implement AI," the instinct is to pick a platform. Which AI tool should we use? Should we try Copilot? Should we get everyone on ChatGPT Plus?

This is the wrong first question.

The right first question is: where is our time going that it shouldn't be?

In most mortgage brokerages, the honest answer involves some combination of the following. Advisers chasing lenders for case updates by phone or email, sometimes multiple times per day. Client information collected at the fact-find being rekeyed into the CRM, then into the sourcing system, then into the lender portal. New enquiries sitting in an inbox or on a spreadsheet, not properly tracked, with follow-up depending on someone remembering. Suitability letters and client communications being written mostly from scratch each time despite following a near-identical structure.

None of this requires a sophisticated AI platform to fix. All of it represents hours per adviser per week that could be recovered. The question is which of these problems is worth solving first, and what the right tool for each one actually is.

That mapping work, understanding where the time goes before deciding what to do about it, is what most brokerages skip. And it's the skip that makes implementation fail.

Why Compliance Adds a Layer Most Brokers Don't Plan For

Mortgage brokerages operate under FCA regulation. That changes the AI conversation in ways that general AI implementation advice doesn't account for.

When you use AI to generate client-facing content, including suitability letters, recommendation summaries, or factual explanations of mortgage products, you retain responsibility for the accuracy and appropriateness of everything that goes out under your firm's name. The FCA has been clear that using AI does not transfer regulatory responsibility to the technology. The adviser, and the firm, remain on the hook.

This doesn't mean AI can't be used for client-facing content. It means the workflow has to include a human review step, and that step has to be documented. AI as a first draft, reviewed and approved by a qualified adviser before it goes anywhere near a client, is a compliant and genuinely time-saving approach. AI generating and sending client communications autonomously is not.

The firms that get this right build the compliance checkpoint into the process before they deploy anything, not after something goes wrong.

Understanding your FCA obligations around AI is covered in more detail in our guide to AI compliance for UK financial services firms.

What Good AI Implementation Actually Looks Like

A client running a small, operationally complex business was spending the first two hours of every working day doing the same thing: opening three separate systems, pulling together the previous day's enquiries and outstanding tasks, and manually working out what needed actioning and in what order. The work itself took a fraction of the time the gathering and sorting did.

The fix was a single automated morning digest: a pipeline that pulled the relevant data from each system overnight, scored and prioritised it according to pre-set rules, and delivered one clear list to the owner's inbox at 7am. By 7:15 they knew exactly what the day looked like without having opened a single system.

The technology involved was not complex. The value was significant. And it came directly from understanding exactly where the time was going before touching a tool.

The same principle applies in a mortgage brokerage. The firms that get real results from AI don't implement AI broadly. They find the two or three specific points in their operation where manual work is most repetitive, most time-consuming, and most predictable, and they automate those points specifically. Everything else can wait.

The result is measurable time recovered per adviser per week, not a vague sense that the business is more modern.

The Three Questions Worth Asking Before Any AI Tool Decision

Before a mortgage brokerage spends money on an AI platform or consultant, three questions cut through most of the noise:

Where does adviser time go that isn't advising? Be specific. Not "admin" as a category but the actual tasks: lender chasing, rekeying, follow-up, report writing. Quantify them if possible. Even a rough estimate per adviser per week is enough to prioritise.

Which of those tasks is repetitive and predictable enough to automate? Not everything qualifies. Tasks that vary significantly case by case are harder to automate well. Tasks that follow a consistent pattern, the same information pulled from the same places in the same order, are the right starting point.

What does compliance require us to keep a human in the loop for? Know the answer before you design any automated process. Build the review step in from the start, not as an afterthought.

Answering these three questions honestly takes a few hours. Skipping them and going straight to tool selection costs months of wasted effort.

Where to Start

If your brokerage has tried AI and found it underwhelming, the most likely reason isn't that AI isn't ready. It's that the implementation started with a tool rather than a problem.

The AI Readiness Score is a free five-minute diagnostic that tells you where your firm sits across the five dimensions that determine whether AI implementation is likely to succeed: process maturity, data quality, operational complexity, compliance readiness, and change capacity. It's a useful first step before committing time or budget to anything more involved.

If the score suggests there's something worth doing, the AI Process Audit is how we find it properly: two weeks, a written report, and a 90-minute walkthrough of exactly where the time is going in your operation and what's worth automating. At £495, it's designed to be a low-friction first step rather than a commitment to a larger programme.

The firms getting real results from AI for mortgage brokers aren't the ones with the most sophisticated tools. They're the ones who did the diagnostic work first.